Updated for the 2025/26 tax year and the changes taking effect from 6 April 2026.

During the COVID-19 lockdowns in 2020, HMRC introduced a number of tax reliefs to support those forced to work from home. Now, several years on, hybrid working has become the norm for many UK businesses. However, the tax landscape has shifted significantly – and a major change is coming in April 2026 that every hybrid worker and employer needs to understand.

The working from home allowance was widely publicised during the pandemic, and millions across the UK claimed it, costing the Treasury an estimated £500m over two years. From 6 April 2022, HMRC tightened the rules, making clear that employees who choose to work from home generally do not qualify. And now, from 6 April 2026, the ability for employees to claim this relief directly from HMRC will be abolished entirely.

What is the Working from Home Allowance?

The working from home tax relief (often called the “working from home allowance”) is a tax relief designed to support employees who incur additional household costs as a result of working from home. It provides a flat-rate deduction of £6 per week (£312 per year) which can be claimed without needing to submit expenses or calculate exact costs.

For a basic rate (20%) taxpayer this is worth £62.40 per year, and for a higher rate (40%) taxpayer it is worth £124.80 per year.

If your actual additional costs exceed £6 per week, you can claim tax relief on the higher amount, but you will need evidence of these costs (e.g. invoices, receipts, utility bills) and must be able to prove they were incurred solely for business purposes.

What’s Changing from 6 April 2026?

In the Autumn Budget 2024, the Government announced it would abolish the ability for employees to claim a deduction from Income Tax directly from HMRC for additional homeworking expenses. This change takes effect from 6 April 2026.

In practice, this means:

- From 6 April 2026, employees can no longer claim the £6 per week flat-rate deduction (or any higher amount) directly from HMRC, whether through Self Assessment or the HMRC online portal.

- The existing employer exemption under section 316A ITEPA 2003 is not affected. Employers can still make tax-free payments to employees to cover homeworking costs.

- This change is estimated to affect approximately 300,000 individuals who currently claim the relief directly.

The key message: from April 2026, if your employer does not reimburse your homeworking costs, you will have no route to claim tax relief on them.

Current Rules for 2025/26 (the Final Year of Direct Claims)

The 2025/26 tax year (6 April 2025 to 5 April 2026) is the last year in which employees can claim working from home tax relief directly from HMRC. The eligibility rules remain as follows:

1. If the employer reimburses the cost of homeworking

Employers can make tax-free payments to help employees cover additional expenses incurred while working from home, under section 316A ITEPA 2003. For these payments to be exempt from Income Tax and National Insurance, both of the following must apply:

- There must be arrangements between the employer and the employee for the employee to work at home.

- The employee must work at home regularly under those arrangements.

HMRC confirms this can apply in hybrid or flexible working arrangements – for example, an employee working at home two days per week. Whilst the arrangements do not have to be in writing, written evidence is recommended.

This route will remain available after April 2026 and is now the only way to obtain tax relief on homeworking costs going forward.

2. If the employer does not reimburse the cost of homeworking (until 5 April 2026 only)

Where the employer does not reimburse homeworking costs, the employee must currently satisfy the more stringent requirements in section 336 ITEPA 2003. HMRC’s guidance is clear that you cannot claim tax relief if you choose to work from home. This includes if:

- Your employment contract lets you work from home some or all of the time

- Your employer has an office, but you cannot go there sometimes because it is full

To qualify, one of the following must also apply:

- There are no appropriate facilities available for you to perform your job on your employer’s premises

- The nature of the job requires you to live so far from the employer’s premises that it is unreasonable to travel there daily.

From 6 April 2026, this route is being removed entirely. Even employees who meet the above criteria will no longer be able to claim directly from HMRC.

What Can You Claim Tax Relief On?

Whether claimed by the employee (until April 2026) or reimbursed by the employer (ongoing), the eligible expenses relate only to additional costs incurred as a result of working from home. HMRC is clear that expenses you would incur anyway (e.g. rent, standard broadband) cannot be claimed.

Expenses you cannot claim

- Council tax – No. This is not an additional cost incurred as a result of home working.

- Mortgage interest – No. This is not an additional cost of home working.

- Water rates – No. Not an additional cost of home working, unless you are on a metered supply (see below).

- Rent – No. This is not an additional cost of home working.

- Broadband / Internet – No, in most cases. This is only claimable if you did not have broadband prior to home working and/or your cost increased as a direct result. If you already pay a fixed broadband rate, no claim can be made.

Expenses you can claim

- Additional telephone costs – Yes. You can claim the additional cost of business calls above your normal tariff.

- Additional heating and lighting – Yes. Compare bills from a home working month against an office month, or calculate on a floor-area basis. For example, if your home office is 10% of your home, you could claim 10% of the additional energy costs.

- Metered water – Yes. Any additional metered water usage directly attributable to working from home.

- Office furniture and equipment – Yes, with conditions. Items must be needed to do your job and there should be no significant private use. It is generally preferable for the employer to purchase equipment directly rather than reimbursing the employee. If the employee leaves or stops home working, equipment must be returned or a benefit in kind will arise.

Capital Gains Tax warning: Property owners should be cautious about claiming business expenses relating to energy or household costs for a dedicated home office, as this can mean that part of the home is no longer eligible for the Private Residence Relief from Capital Gains Tax. This can have significant tax implications, particularly if the property is your primary residence.

How to Obtain Relief: Your Options

Option 1 – Employer pays £6 per week (recommended, available now and after April 2026)

Employers can pay employees up to £6 per week (£26 per month) tax-free to cover increased costs of working from home. No records or receipts are required at this level. This is processed through payroll and must be excluded from tax and pension deductions.

If the employer wishes to pay more than £6 per week, they may do so but will need to keep records and supporting documentation for the amounts claimed.

This is the route that all hybrid workers and their employers should focus on from April 2026 onwards, as it will be the only mechanism for tax-free homeworking payments.

Option 2 – Employee claims directly from HMRC (available until 5 April 2026 only)

For the 2025/26 tax year and earlier, employees who meet the eligibility criteria and whose employer does not reimburse them can claim through their Self Assessment tax return or the HMRC online portal. Claims up to £6 per week do not require supporting documentation.

Important: Check your payslip before claiming. If your employer already pays a homeworking allowance, submitting an additional claim would be double-claiming.

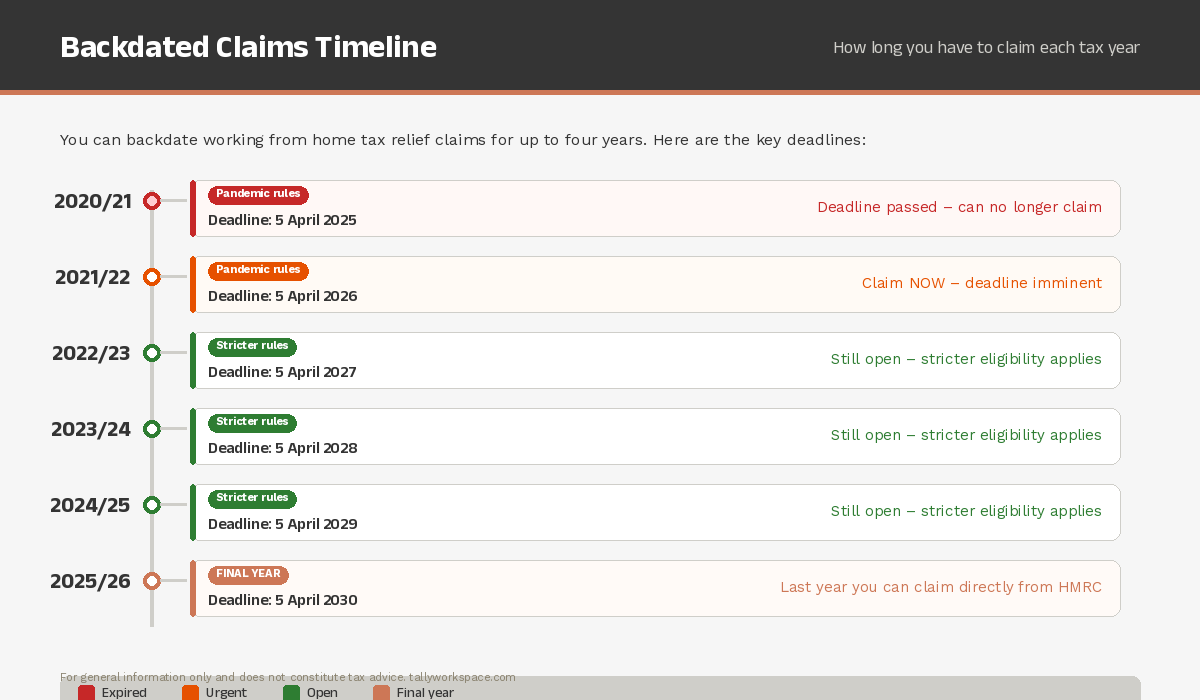

Can You Claim for Previous Years?

Yes. HMRC allows you to backdate claims for up to four years, provided you met the eligibility criteria at the time. The current deadlines are:

• 2021/22 tax year – claim by 5 April 2026

• 2022/23 tax year – claim by 5 April 2027

• 2023/24 tax year – claim by 5 April 2028

• 2024/25 tax year – claim by 5 April 2029

• 2025/26 tax year – claim by 5 April 2030 (final year of direct claims)

Note that for the pandemic years (2020/21 and 2021/22), the eligibility criteria were more relaxed. From 2022/23 onwards, the stricter rules described above apply.

Action for Employers

With the abolition of direct employee claims from April 2026, employers offering hybrid working arrangements should consider whether to introduce (or continue) a tax-free homeworking payment of £6 per week through payroll. This is a low-cost way to support employees, requires no additional record-keeping at the flat rate, and will be the sole mechanism for homeworking tax relief going forward.

Employers providing equipment (such as office furniture, monitors, or an internet connection) for employees to do their job at home can continue to do so without creating a tax liability on the employee, provided private use is insignificant.